TSMC Stock: Why This Semiconductor Giant is My Highest-Conviction Buy

Ultra Deep Dive (7,400 Words) on Why TSMC (NYSE:TSM) Has a 95% Upside and a Near Monopoly on Advanced Chips

In Romy and Michele's High School Reunion (1997), there is a scene that was a very common dynamic in high school. Romy excitedly gets invited to prom by a guy, but later, he cancels on her because one of the popular girls becomes available. It’s a classic case of ditching someone for a more desirable option.

I have to admit that I was that guy, and TSMC (Taiwan Semiconductor Manufacturing Company Limited) was Romy.

I remember the first time I bought TSMC was in 2015, when the shares were trading around $20, as my TD Ameritrade was transitioned to Schwab, I don’t have the historical trade, but I believe I sold it for a slight gain, maybe at $28 per share.

Why did I sell?

Because I doubled down on another name that I saw as more attractive. The same thing happened in 2021; I bought the shares at over $100, and I lost money when I sold them in 2022 at $80 per share.

Why did I sell?

Again, I found a better opportunity.

I bought TSMC shares again last year,

I entered at $196 and the position is 1.0% of the portfolio.

So with the Trump saga, I have been reviewing my portfolio. I was surprised that instead of selling TSMC to buy a better opportunity, this time TSMC was the better opportunity—TSMC is not my Romy anymore!

Earlier this week, I sent a trade alert to paid subscribers to start divesting (RCL, RGA and BLBD—my new Romy) and reallocate that capital to TSMC. As I have no idea when the bottom is in this market, I advised a weekly dollar-averaging, reallocating 0.5% of the portfolio from those names to TSMC.

In this post, I will go over why I think TSMC is the best opportunity out there in the current scenario. This has been one of the easiest stories I had to write, as it is a textbook example of a company with a wide moat.

I see the fair value of the shares at $338, a 95% upside from current levels.

How come your strongest pick offers just a 95% upside?

Yes, it is just 95% but it is my highest conviction pick. Sure, I have other names that are multi-baggers on my list, such as QUBT, but my conviction is not as high and the downside is way lower. True, TSMC could be worth ZERO if China invades Taiwan and the market is assigning a non-zero probability to that scenario. But I see that scenario as a very, very, extremely very unlikely scenario. So my bear scenario is not zero but $110. (I later explain why $110 but if you can’t wait just go here)

I went overboard on this deep dive but here is the elevator pitch:

TSMC has a technical monopoly on the most advanced chips in the world. TSMC has pricing power and the demand for those chips will explode driven by the increased demand for AI, cloud services and EV adoption. I value the shares at $338, a 95% upside from current levels. The opportunity exists because the market is discounting the stock price to account for the China risk. The market thinks China taking over Taiwan is a real risk. I believe that risk is overblown as the US won’t allow China to conquer Taiwan.

If you are sold on the pitch, then no need to read the deep dive, but if you disagree with any of my claims or are just curious, keep on reading.

As the thesis is long (over 7,400 words), I have created the table of contents below so you can jump to the section that most interests you.

Why topline growth will accelerate (price x volume)

Fair share price of $338 (valuation)

The China risk and other risks (thanks goes to my friend MJ who did a great job challenging my assumptions on the China / Taiwan conflict)

Let’s dive in 🤿!

TSMC, the gem of the industry

TSMC (NYSE: TSM) is the leading global semiconductor foundry, holding a dominant market share of approximately 70%. TSMC manufactures legacy nodes (28nm+) and advanced nodes (7nm to 3nm).

While TSMC has a 50% market share in the most common semiconductors, it has 90%/80% of the 3nm/5nm semiconductors market, the most advanced semiconductors. In advanced chip production, TSMC effectively holds a monopoly with cutting-edge manufacturing processes offering substantial performance and efficiency improvements (e.g., 15-20% performance gains or 30-40% better power efficiency with each node advancement).

The company manufactures for major chip designers such as NVIDIA, AMD, and Integrated Device Manufacturers (like Intel). Revenue streams include merchant card fees, smartphones, consumer electronics, automotive, IoT, and digital consumer electronics, among others. Recently, TSMC expanded into in-house packaging technologies (such as CoWoS), crucially enhancing its ability to control costs and pricing.

TSMC’s core strengths include its market-leading proprietary technology and deep customer integration. These create a robust competitive moat reinforced by scale advantages, enabling substantial R&D investments, further widening the technology gap over competitors like Samsung and Intel.

Accelerating Top-line Growth Trajectory

In simple terms, sales are the multiplication of price times quantity (unit sold). In the case of TSMC, I argue that revenue growth will be driven by both price increases and more units sold.

Let’s talk quantity.

The rising adoption of cloud services, AI workloads and sophisticated gaming will increase the demand for advanced-node chips. Yes, those are the chips where TSMC has a 90% market share.

Modern data centers and cloud servers heavily rely on advanced semiconductors for high-performance computing such as machine learning, big data analytics, and cloud storage solutions. For example, NVIDIA’s GPUs, critical for AI workloads and deep-learning models, are almost exclusively manufactured by TSMC, particularly using TSMC’s advanced CoWoS packaging technology.

Just to give you an idea of how many chips are needed, each server rack may contain dozens of GPUs. A general-purpose server would have 1 GPU, a high-performance computing server would have 2 to 4, and an AI/ML training server would have 4 to 8 GPUs.

Hyperscale data centers, think of Amazon’s AWS, Microsoft’s Azure or Google’s GCP, are enormous consumers of advanced chips, each deploying tens to hundreds of thousands of TSMC-manufactured chips annually. While a small Hyperscale datacenter could have 50,000 servers, a large one would have more than 1 million servers. So the demand for chips could be as much as 8 million chips per large data center.

Gaming consoles, such as Sony's PlayStation 5 and Microsoft's Xbox Series X/S, heavily rely on TSMC-produced AMD custom-designed CPUs and GPUs. For example, the PS5 and Xbox Series X consoles utilize TSMC's 7nm process technology for their central processors. Each generation of console ships tens of millions of units.

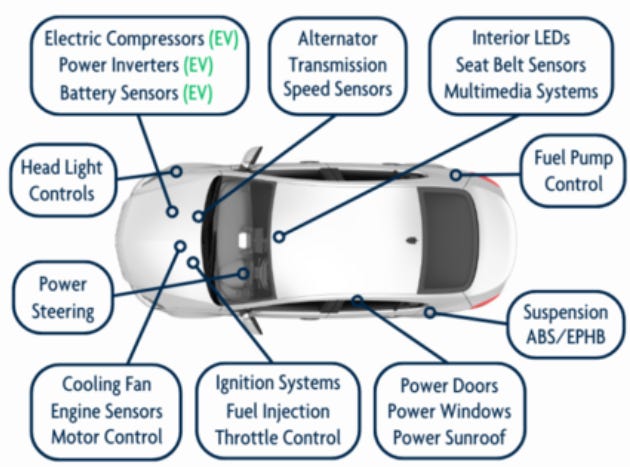

And this is just the trend on the advanced nodes, but also the EV trend will increase the demand for chips.

ICE vehicles use 800 to 1,000 chips to control various things like the engine, transmission, airbags, ABS, navigation, powertrain and lights. However, an EV uses 2-3x more chips than an ICE mainly for batteries, power electronics, motors, advanced driver assistance, connectivity and autonomous driving in such models such as Tesla. On top of that, EVs require more sophisticated chips than ICEs. So it is a double benefit for TSMC; more chips of the ones where TSMC has 90% market share.

And don’t get me started with autonomous humanoid robots…but I hope you get the idea by now.

I want to save enough money to buy one of those Tesla Bots when they come out, I am lousy at folding laundry 🙈

TSMC has considerable pricing power

As per the price of those chips, management has adopted a stronger stance on exercising pricing power, this allows TSMC to capture a greater portion of the AI chip value chain as competition intensifies. And I don’t think clients can push back as they have no alternatives to TSMC.

Deep customer integration and tailored manufacturing processes dramatically increased switching costs, effectively locking in long-term demand. Each technology node developed by TSMC is specifically adapted in collaboration with its clients, which makes it extremely difficult and costly for customers to switch foundry suppliers.

Very likely TSMC's clients will pass through the cost to their customers who won’t even register the price.

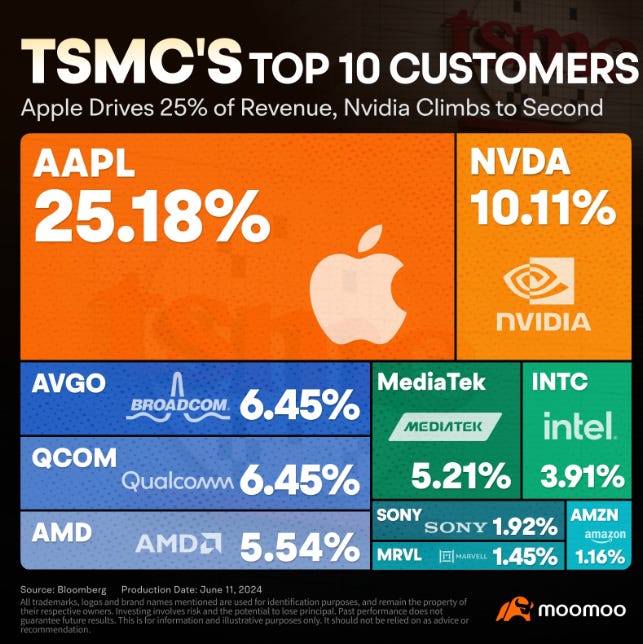

Let’s take Apple’s example.

Apple generates 25% of TSMC's revenues, or $22.0 billion in 2024 (25% of TSMC’s 2024 revenues of $88.1 billion). That would represent 10.5% of Apple’s COGS of $210.3 billion.

Remember this is just an estimate. First off, the fiscal years for Apple and TSMC are phased by three months and I am assuming that all TSMC’s costs are direct and accounted for in COGS and none in SG&A.

If TSMC increases prices by 10%, Apple would have an incremental cost of $2.2 billion (10% x $22 billion).

In 2024, Apple sold approximately1 297 million units (230 million iPhones, 30 million Macs and 37 million iPads). Assuming that each unit has the same concentration of chips (which it doesn’t), the increased cost per unit would be $7.40 per unit. That incremental cost wouldn’t even register with Apple customers paying over $1,000 per iPhone, Mac or iPad.

But Apple uses mainly the 5nm chips, what about the 3nm?

AMD has been transitioning its product lines to TSMC's advanced process nodes. Notably, AMD's Zen 5 architecture is designed with both 4nm and 3nm processes in mind. AMD generates $4.9 billion of revenues for TSMC (5.54% of revenues) which is a whopping 40% of AMD’s COGS of $12.1 billion.

A 10% price increase would be an increase of 4% in AMD’s COGS or $480 million. AMD doesn’t release the units sold but if we assume an average selling price of $350, AMD would have sold 73.7 million units in 2024. The $350 is a pure guestimate as AMD chips sell in a wide range from $849 for an Athlon 700, $549 for a Radeon RX 9070 to $275 for an FX-8170 processor.

So the $480 million incremental cost would be only a $6.51 increment per unit. Again, irrelevant for a customer buying a $275-$849 chip.

And even if customers were unhappy, if they want the tech with the latest and best-performing chips in our known universe, they have to pay as there is no alternative.

Diving even deeper into TSMC’s Competitive Advantages

Back in 2003 while in engineering school, I was into battlebots and one of my favorite battlebots was our below creation (I forgot its name as it was 22 years ago and I don’t even remember what I had for dinner yesterday).

We didn’t win, but it was fun. Here is a video of that fun tournament.

Enjoy!

While I don’t remember the exact chip we used to program the battlebot, the most used chip in those days was the 0.13µm (or 130nm).

We have come a long way from those days.

TSMC manufactures chips from 250nm down to 3nm. Historically the ‘nm’ referred to the transistor’s gate length but today is more of a marketing term to differentiate generations. What you need to know, the smaller the number, the smaller the transistors and the more advanced the technology. So for example, the 130nm chip I used in that battlebot would have 1.5 million transistors per square millimetre. That is tiny, the tip of a sharp pencil is 1 square millimetre. On that tip there would be 1.5 million transistors…and that is the old technology.

Now let’s talk about 2023’s technology, the 3nm. Guess how many transistors it can fit on the tip of that pencil.

Take a wild guess.

250,000,000 to 300,000,000 transistors.

Hard to imagine? You are not alone, check this out 👇🏽

Each new generation is more power efficient and faster. For example, 3nm nodes are 30% more efficient and 15% faster than the 5nm nodes. As each node shrinks the size of transistors, smaller transistors require less voltage to switch on and off, reducing power consumption. Also, a smaller transistor means more transistors can be fit in the same space, which means electrical signals travel shorter distances improving processing speed. Also, more transistors in the same space means more processing power in that area. Finally, engineers have introduced new transistor architectures such as FinFET and GAAFET to solve efficiency problems.

As you can tell by now, manufacturing chips requires a lot of technology. Technological leadership in this space is not chip (oops I meant cheap). TSMC has been spending around $30 billion a year just in capex, not to mention R&D which I will explain later.

That money is deployed to build new fabs, purchase lithography machines and increase production capacity.

A semiconductor fabrication plant, also known as a fab, costs between $10 and $28 billion. Those fabs are expensive as the facility must be ultra clean (1000x cleaner than a hospital), require precision tools to print transistors on a nanoscale, and the facility requires advanced cooling and chemical processing systems. And each newer generation seems to be more expensive, for example, TSMC’s Arizona fab (4nm, 3nm process) costs around $16 billion2 while TSMC’s Taiwan 2nm fab is expected to cost up to $28 billion.

Extreme Ultraviolet (EUV) Lithography is the core technology allowing chips below 7nm and each machine costs around $380 million. For example, a 3nm production line would have 20 to 30 EUV machines just in one fab.

Finally, TSMC is increasing its capacity to meet demand. As I explained, demand for advanced chips is exploding, so TSMC needs to build more capacity and is expanding in Japan, Germany and Arizona.

Shouldn’t TSMC repurpose legacy node fabs or even 7nm fabs for new generations?

That is not feasible for two reasons, there is still demand for legacy nodes and fabs cannot be repurposed.

The legacy nodes (28nm, 40nm, 65nm…) are still used in TVs, washing machines, cars and industrial equipment. Basically, anything that needs a chip but doesn’t need high computing power. They are cheaper and easier to make so it makes sense to use them where high computing power and power efficiency are not an issue such as in your microwave.

Secondly, and more importantly, the fabs cannot be repurposed due to the technology used. Different nodes require different lithography technologies. A 7nm fabs use Deep Ultraviolet Lithography (DUV), while 3nm requires Extreme Ultraviolet Lithography (EUV). Old fabs wouldn’t have the extra space or infrastructure to accommodate new EUV machines unless you rebuild 80% of the facility making it almost as expensive as building a new fab.

Also, the cleanliness requirements for 3nm are far stricter than for 7nm. The 3nm transistors are smaller, so even a tiny particle can cause defects. Older fabs’ air filtration and contamination control systems are not good enough for extreme miniaturization.

Another factor is that smaller transistors (3nm) need different voltages (~0.6V vs. 0.75V for a 7nm) and power distribution networks. Power delivery needs to be ultra-precise, or chips won’t function reliably. Ultimately, the 7nm fabs were not built with the extreme precision needed for 3nm power supply networks.

Finally, fabs are designed with fixed tool layouts, wiring channels, and gas & chemical flow systems. Different chemicals are used by 3nm and 7nm, requiring a different infrastructure. Even if TSMC repurposed an old fab, they would need to rip out a huge amount of equipment.

Besides capex, TSMC spends $6 billion in R&D annually.

I think this level of R&D is critical to stay ahead. This R&D is allocated to developing smaller and more efficient nodes, pioneering new chip architecture, improving yield, reducing defects, 3D stacking and advanced packaging. For example, TSMC spent years perfecting 3nm GAAFET transistors before mass production in 2023.

In a nutshell, to play in this space and be the leader, you need to cough up $36 billion…each year, good years and bad years. On top of that, spending that money doesn’t guarantee the development of the new generation chips nor does it guarantee you will have sufficient clients to justify the investment. That is what happened to GlobalFoundries when it exited the race in 2018.

In 2018, GlobalFoundries decided to halt its development of 7nm and more advanced chips. The main reason was financial viability—there weren’t enough customers to justify the massive costs. This was especially true as fewer fabless clients were adopting these cutting-edge nodes, which required substantial investment.

Instead, GlobalFoundries chose to focus on refining and expanding its legacy node processes, targeting fast-growing markets like IoT, 5G, automotive, and industrial technologies. The move was seen as a pragmatic decision, especially as the competition in advanced nodes was narrowing to companies like TSMC, Samsung, and Intel.

Now there are three competitors left on paper: Intel, Samsung and TSMC. But Intel is not even competing (more on that below) and Samsung has a 10% market share in the 3nm nodes leaving TSMC running a technical monopoly.

This industry is designed for few players

This dynamic reminds me of my telecom days and how the economics of the industry is structured for few players.

Years ago I ran corporate development for the largest telco in Chile. Part of my role would be to advise on the price we would bid in the public auctions for broadband spectrum. In Chile, it would be a combination of a payment to the government plus a commitment such as bringing connectivity to the far-reaching rural areas. Those auctions were expensive.

Let’s take the 2021 5G auction, Entel paid $143 million for the 3.5 GHz spectrum plus Entel committed to expand coverage to cover 318 communities and provide service to public institutions. The capex on that coverage commitment is not cheap.

Besides acquiring the spectrum and spending on honouring the coverage commitments, Entel had to invest in new RAN equipment and densify the telecom antennas in the case of 5G. That is a lot of money, and that large investment had to be made with each new wave. It happened when telcos went from 2G to 3G, then from 3G to 4G and now from 4G to 5G.

The only way to justify the investment would be if you have a large customer base, which is why you only have three to four telecom competitors per country. MVNOs such as Virgin Mobile and Freedom Mobile don’t count as they are just a marketing platform renting the infrastructure from the big players.

I see the same scenario here, to justify the $36 billion annual investment, you need to capture a significant portion of the demand. Who will invest $36 billion hoping to capture 30% of the market?

So even if you are willing to invest that money and somehow you have guaranteed clients, you still need to get the technology right, be able to execute and deliver.

Why Intel is not a competitor to TSMC in advanced chips

I think now is a good time to talk about Intel. Intel is falling way behind in the race and as a consequence, it was forced to get advanced chips from TSMC just to survive. Intel had many missteps causing it to fall behind. Let me try to summarize them:

Misstep #1. Delayed adoption of EUV lithography

Intel tried to extend the usage of DUV lithography while TSMC and Samsung were already adopting EUV lithography for 7nm. By the time Intel finally recognized its mistake and incorporated EUV for 7nm, TSMC was already at 3nm.

Misstep #2. Process issues

While TSMC shipped 7nm in 2018 and 5nm in 2020, Intel’s 10nm node was delayed by 6 years due to yield and performance issues. Intel was too aggressive on transistor scaling leading to a too complex process that was hard to mass-produce. By the time Intel fixed its issues and launched its 10nm node in 2021, it was already obsolete as TSMC was on the 5nm by then.

This delay also pushed the 7nm from 2021 to 2023 which had defects and required major redesigns. So when Intel launched its 7nm in 2023, TSMC was ramping up 3nm.

Misstep #3. Poor foundry model and rigid manufacturing

Unlike TSMC, which only fabricates chips for customers, Intel both designed and manufactured its own CPUs. TSMC was built to scale by producing for Apple, NVIDIA, AMD, Qualcomm, etc. Intel’s fabs were optimized for its own CPUs, making them less flexible for a foundry business.

In 2021, Intel decided to become a foundry. However, its fabs were not optimized for outside customers. TSMC has decades of experience running a foundry, whereas Intel is still learning.

Misstep #4. Bad financial management

Intel’s fab construction and upgrades have been slower and more expensive than planned. Intel’s Arizona & Ohio fabs (for 7nm and below) are taking longer than expected. Meanwhile, TSMC builds fabs faster and at a lower cost due to years of foundry experience.

These four missteps have hurt Intel. Apple switched from Intel to TSMC for Mac processors in 2020. AMD now relies entirely on TSMC for Ryzen CPUs, gaining market share over Intel. And NVIDIA designs its own GPUs but manufactures them at TSMC because Intel’s fabs were not advanced enough.

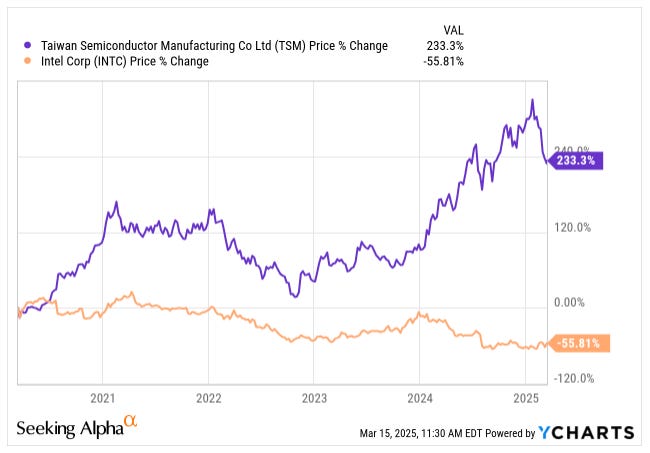

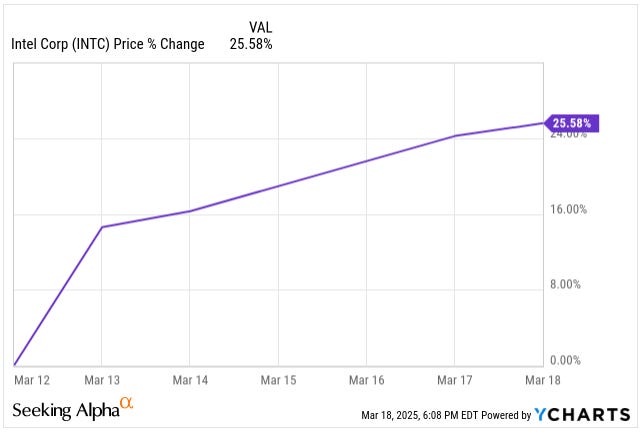

No wonder Intel’s stock has more than halved in the last five years while TSMC’s more than tripled.

Finally, Intel is changing its CEO. On March 12, the company announced Lippu Tan as its new CEO, entrusting a seasoned semiconductor industry veteran and former board member with one of the most challenging roles in the industry.

Lippu Tan is a well-respected industry veteran, currently 65 years old, who initially entered the semiconductor world as a venture capitalist before transitioning into leadership roles. He later became CEO of Cadence Design Systems, where he successfully rescued the company from a difficult period and built his career there. It seems that his defining characteristic is his extensive network of contacts—he is well-connected with key players and companies across the semiconductor industry. Intel is hoping that these connections will be instrumental in shaping its future strategy.

Will Lippu Tan Change Intel’s Strategy?

So far, we don’t have a clear answer. Based on the public statements, it appears that he will continue along the same strategic path as the previous CEO, Pat Gelsinger. However, as of March 18, the shares of Intel are 25.6% up, the markets believe that he will unlock value, potentially through splitting up the company—something Gelsinger strongly opposed. It remains to be seen whether Tan will stick to Intel’s existing roadmap or explore alternative strategies.

One key area where Tan's extensive industry network could make an impact is in attracting outside customers to Intel’s foundry business. Intel desperately needs more external clients to use its manufacturing services. If Tan can successfully leverage his contacts to convince these companies to work with Intel, it could be a major turning point.

There has been speculation that Intel could collaborate with TSMC for its foundry services, particularly following a Reuters report suggesting that TSMC pitched a joint foundry venture with Intel to NVIDIA and Broadcom. If Intel is to remain competitive, it must secure substantial external orders.

For Intel to succeed, it needs to rebuild its reputation and persuade major chip designers to trust its manufacturing processes. Historically, Intel was seen as a dominant, closed-off player, but now it must position itself as a flexible and reliable foundry partner. I don’t see how chip designers will leave TSMC to go to Intel, once you invested the time and money to design chips for the TSMC process, it makes no sense to go back to the drawing board and redesign chips for the Intel process. Especially as Intel has had many missteps while TSMC has shown just pure excellence to its clients.

That is why I see TSMC's customer relationships as another wide moat. TSMC’s foundry model—where customers collaborate closely on process technology—results in deep integration and tailored manufacturing solutions. This deep collaboration significantly increases customer switching costs, further insulating TSMC from competitive pressures.

One of the biggest concerns is Intel’s planned $30 billion investment in a fab in Ohio. Intel has made it clear that it will only proceed when the demand justifies the investment. Observing the current market dynamics, I see it extremely unlikely that Intel will secure those clients.

The $30 billion investment is a big bet for Intel. Currently, Intel is generating $8.3 billion in cash flow from operations while deploying $24 billion in capex. This required Intel to close the gap with debt. Currently, it has $50 billion in debt and $23 billion in cash.

How much more debt can Intel take up on this gamble?

If Tan is a rational CEO, he should raise the white flag and admit that Intel is past its prime and will gradually decline. However, Intel remains a massive company—even if it scales back its ambitions, it could still be a profitable business, just not the dominant player it once was.

But Tan doesn’t have lots of time, the clock is ticking, debt is racking up and TSMC is already working on 2nm. If Intel continues with its aggressive turnaround strategy without success it can turn ugly. However, if the company adopts a more conservative approach, it could survive without urgent pressure.

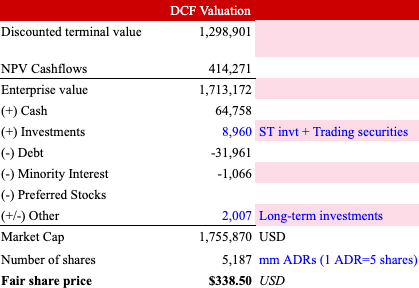

TSMC’s fair value is $338 per ADR

I value the ADRs at $338 using a DCF model.

Note that from now on when I show figures from the financial statements, they are in New Taiwan Dollar (~33 TWD = 1 US Dollar). The model is in USD and I made the respective changes in the cost of capital. Finally, note that five shares are equal to one TSMC’s ADR (the ones trading on the NYSE). There is a current 18% arbitrage opportunity between the ADRs and the shares, however doing the arbitrage seems not possible due to investor restrictions (but if you figure out a way to do it, let me know 🤣).

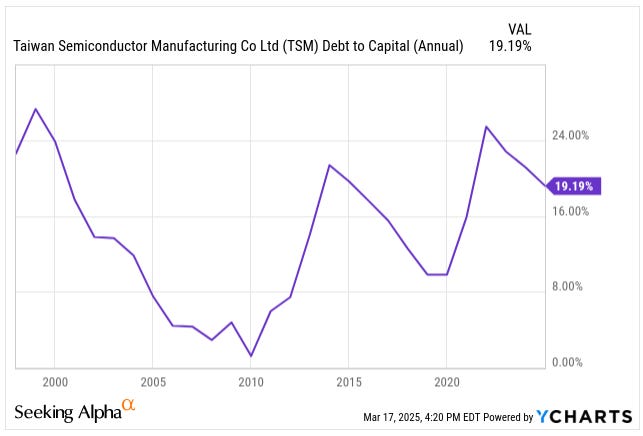

The cost of capital utilized is 9.4% based on an unlevered beta corrected for cash of 1.46 for the semiconductor industry and an optimal debt-to-capital ratio of 40%. TSMC has been operating with a very low debt-to-capital ratio of around 20%

As it doesn’t make sense for the company to grow by acquisitions (no one can build fabs as good as them), and they have not done any significant share repurchases, the only extra cash has been allocated to dividends (which they could increase) and organic growth (building new fabs).

However, I expect the company to eventually start buying shares or increase the dividends as the current cost of capital base is inefficiently high (11.30% vs. a 9.40% optimal cost).

Below are my main assumptions, but I will dig deeper into the main ones.

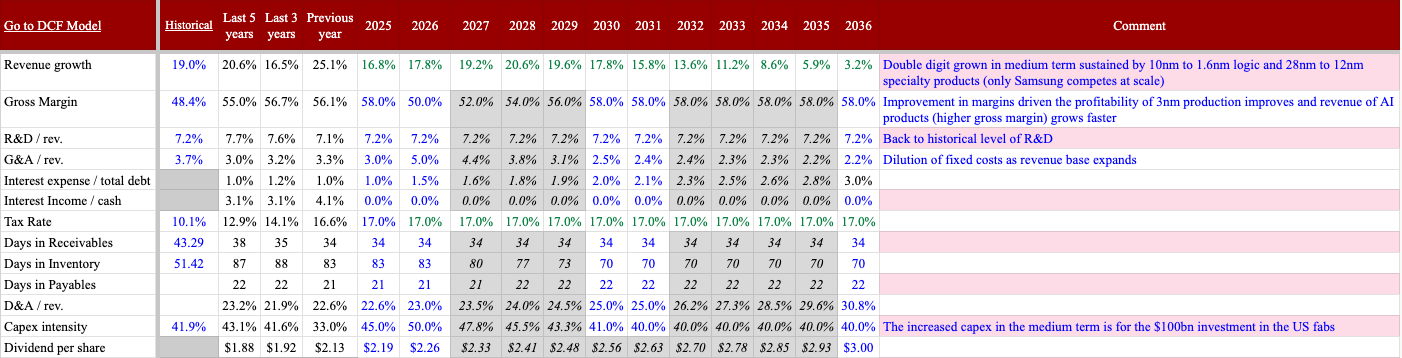

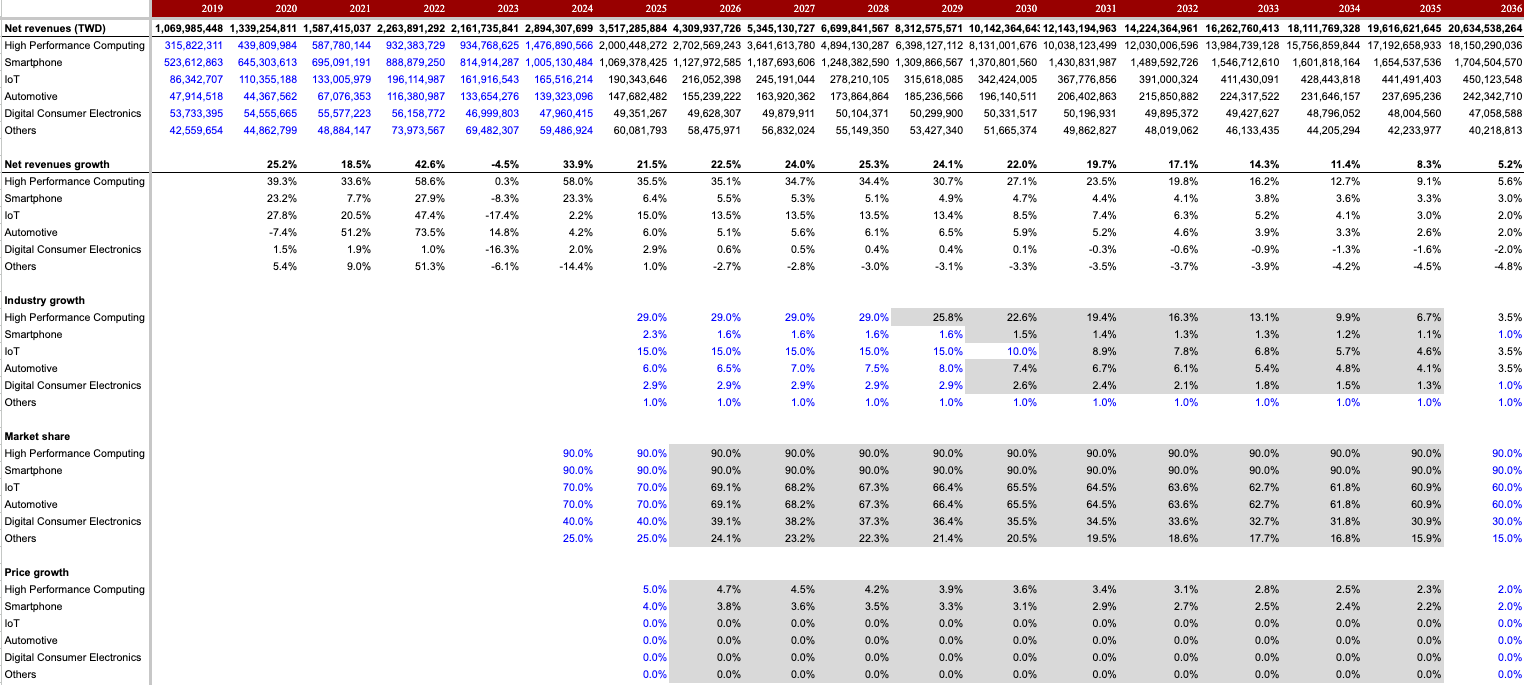

Revenue growth to stay high due to market dominance, pricing power and strong industry fundamentals

I expect revenues to stay above 20% till 2030 and then gradually decrease. There is a triple factor happening here, the industry is rapidly growing, TSMC has a dominant share in the right segments and it has the power to dictate price increases.

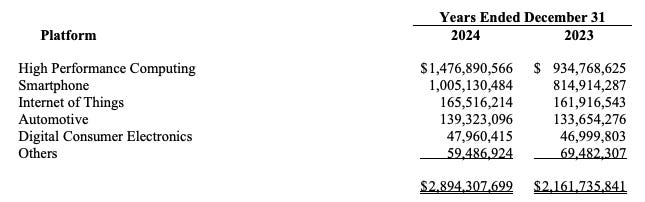

High Performance Computing (HPC) and smartphones use 5nm and 3nm in which TSMC has 90% market share. Internet of Things (IoT) and Automotive mainly use 28nm chips where TSMC has a 70% share and for consumer electronics, we can assume they use the chips where TSMC has a 40% share.

While I expect TSMC to maintain its market share in HPC and smartphones, I assumed TSMC would give up some share in IoT, automotive and consumer electronics eventually decreasing to 60%. One possible scenario is that if Intel gives up the hopes to compete in advanced chips, it may focus on this sector with its existing fabs. In that scenario, it would make more sense for TSMC to focus on the advanced chips rather than entering a price war.

As per pricing, I only assumed price increases in advanced chips, TSMC already spoke about increasing 3nm prices by 20%, but here I assumed a more steady increase.

For HPC, I used the IDC forecast for AI growth and smartphones. As newer phones have more chips to do more things, the growth of smartphone chips should be higher than the growth of smartphones. For example, the newest iPhones have chips for facial ID, separate chips for connectivity and a neural engine chip. I expect the trend to continue. However, for the valuation, I assumed smartphone chip growth would be the same as smartphone growth.

For IoT and consumer electronics, I based my forecast on Statista and EPT respectively.

After the forecasted period for each segment, I assume a gradual deceleration. While a good assumption for most segments, it is a conservative one for HPC. We can separate HPC demand into training and inference. Training is the initial, heavy-duty computing needed to create large AI models (like ChatGPT). Training needs massive computational power. Inference is the everyday use of trained AI models (answering questions, image recognition, autonomous driving, etc.). Inference can often run efficiently on smaller, less powerful chips. So the HPC growth is initially driven by the demand for chips for training, this will slow down and eventually flatten once the models become sufficiently powerful. But inference will continue growing rapidly because inference is embedded into everyday devices (phones, cars, appliances, etc.). So even after the forecasted period, HPC demand should be higher than I forecasted as more and more everyday devices become AI-powered.

Also, Edge computing, that is, running AI applications directly on local devices (phones, sensors, robots, smart home devices) instead of in centralized data centers, should grow massively because AI devices will become mainstream and replace many human jobs over the next 5–10 years. This additional pickup in demand is not included in the valuation, think of it as a margin of safety.

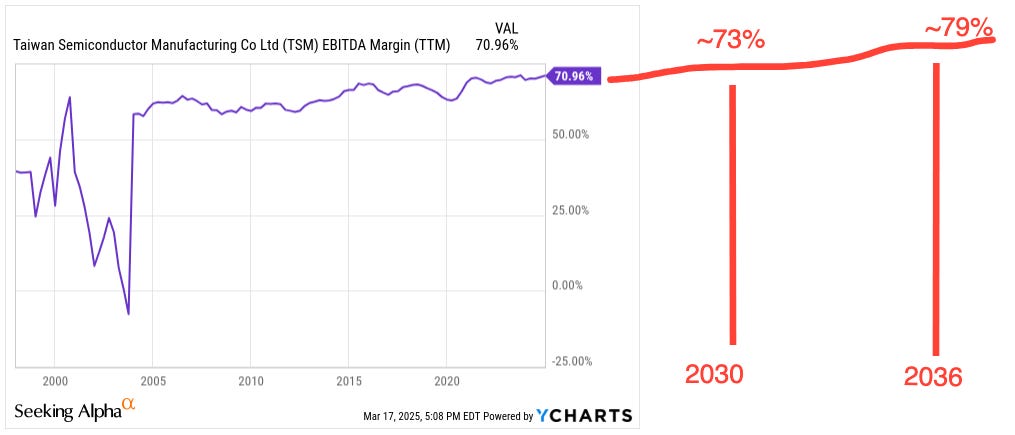

Margins to keep improving

Going into detail about margins was difficult as the cost of sales was not opened up in the financial statements. However, we can triangulate into a margin that makes sense. I expect margins to gradually improve reaching a peak close to 79% by the end of my forecasted period.

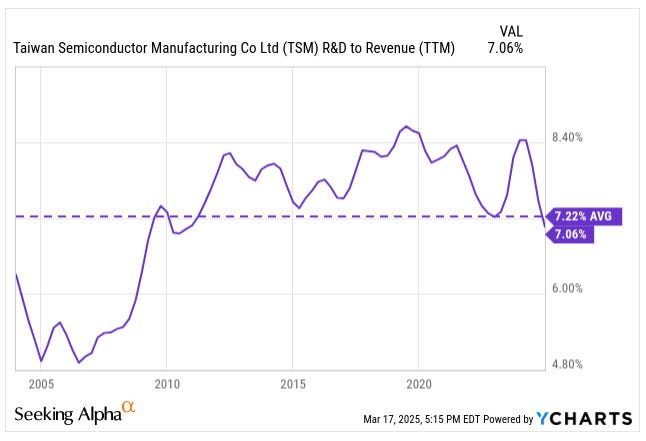

TSMC knows the value of being the technological leader so I am confident they will continue pumping into R&D. I assumed they will continue to invest 7.2% of its revenues into R&D.

You might say that since 2010, TSMC has invested more than 7.2% of its revenues in R&D, but I think we should focus on the absolute dollar amount. In 2024 they spent $6.2 billion in R&D, this forecast includes $9.4 billion for 2026 and $45 billion by 2036, just insanely high numbers. If at all, I expect R&D to decrease in the coming years as the numbers are so high and it may be difficult to deploy all that money.

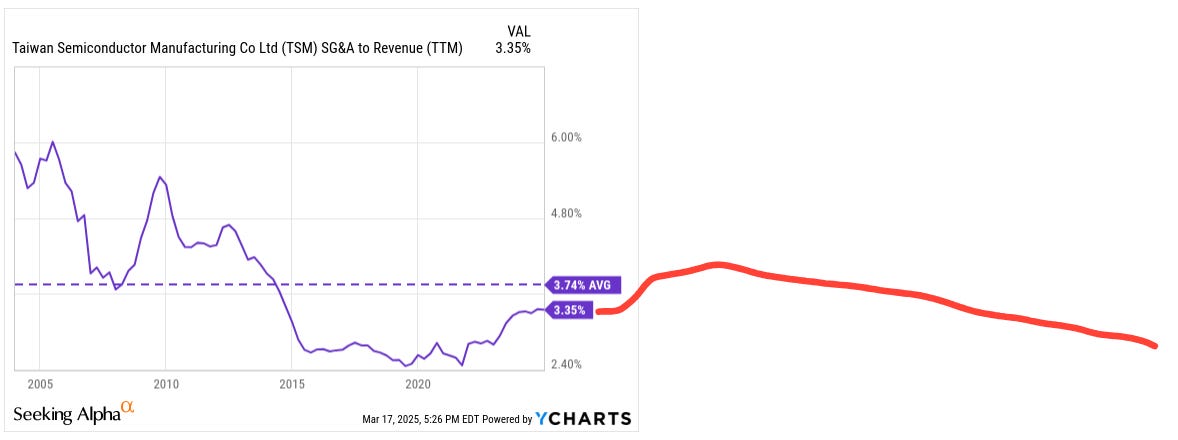

As per SG&A, I expect an increase in the short term as they will be building support functions for the new fabs in the US. However, I expect the percentage to decrease gradually as the top-line growth would dilute fixed costs. Again, in absolute terms, SG&A still increases from $2.9 billion in 2024 to $13.7 billion by 2036.

Gross margin was the most difficult to forecast because the margin should improve as 3nm production improves and as advanced chips (higher margin) compose a higher portion of TSMC’s revenues. However, on the other side, I see competitive pressures on the other chips and also I think whatever chips are produced in the US are at risk of being sold at a lower price.

So I backed into a gross margin by lowering the return on invested capital (ROIC) of the $100 billion that would be invested in the US. I assumed the ROIC higher than the cost of capital, but not as high as the ROIC of the rest of TSMC’s invested capital.

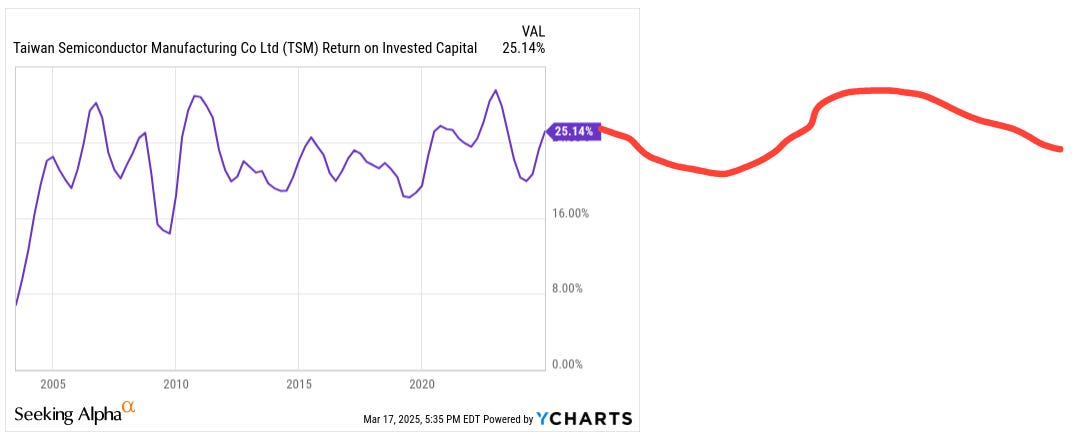

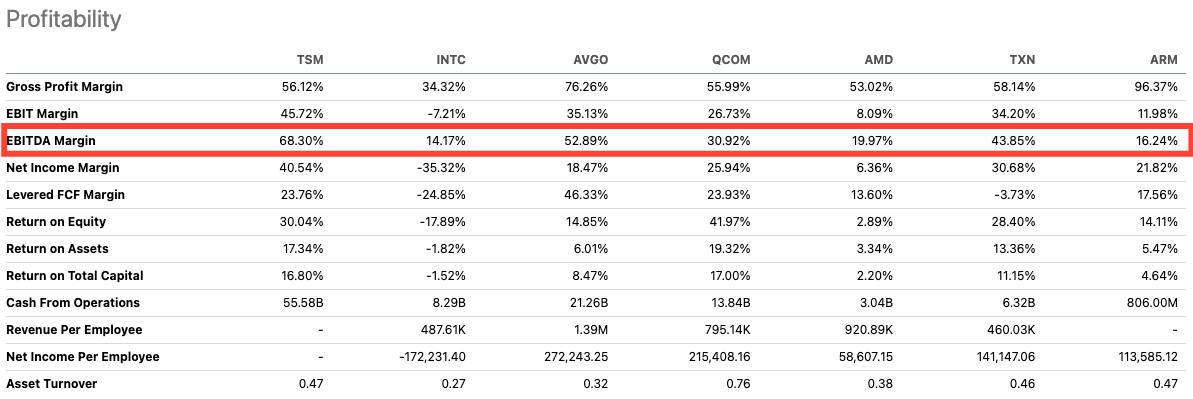

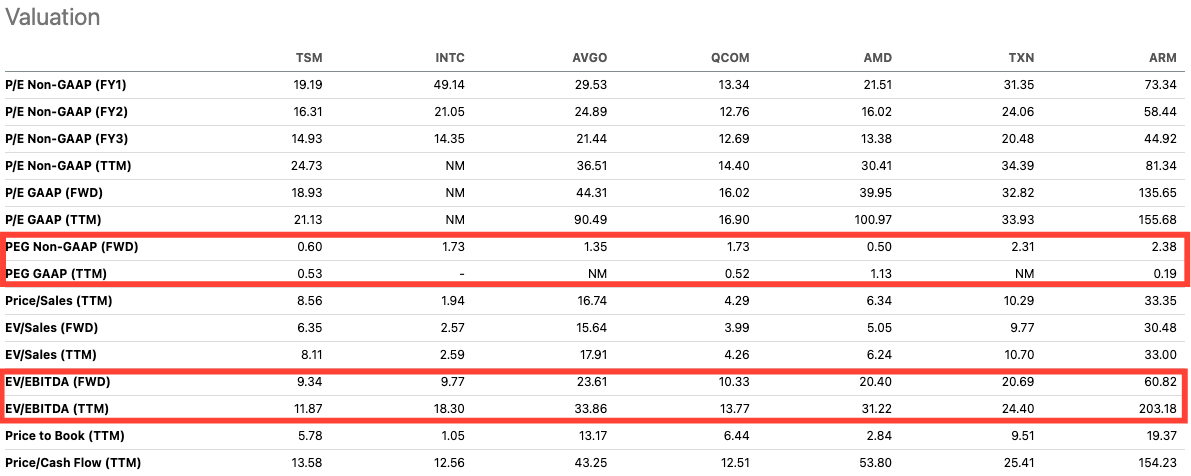

On a relative basis, TSMC is the most profitable and cheapest company among its peers. Its EBITDA number has reached escape velocity and as I mentioned earlier, I expect the margin to continue expanding.

On a PEG basis, the price you are paying for a dollar of earnings adjusted for growth is 60 cents—a steal. Also if you look at EV/EBITDA, it is the lowest multiple among peers.

So you are paying a discount for the gem of the industry, not a bad deal at all.

What are the ADRs worth in the worst scenario?

I know many people say that the worst scenario is China invading Taiwan (TSMC shares are worth zero), but as I argue in the following section, that risk is too improbable and if it happens we would have bigger problems.

The worst case scenario in my books is if TSMC faces real competition, be it Intel, Samsung or some disruptive company we don’t know about. I think all of those are very unlikely but if it happens I value the shares at $110.

I had a scenario where the demand was not as high as I forecasted, however, with that scenario, the shares were worth $132, so my worst scenario is due to competition, not due to lower AI-related demand.

In a competitive scenario, first TSMC would lose some market share, then some more and then they would retaliate by lowering prices, to which the competitor would respond with even lower prices. That price war would continue until ROIC would be equal to the cost of capital. So when I play with margins to obtain ROIC, the average of the different scenarios to come to that ROIC equates to $110 per share.

Risks

I included the risks to make this thesis more balanced. I think the market is discounting the share price due to these risks (mainly Risk #1).

Risk #1. China taking over Taiwan

When talking to investors, reading analyst reports and backtracking the implied risk premium at the current share price, it is evident that the market considers China invading Taiwan a valid concern. But this risk premium is overblown.

I think China acknowledges the strategic value of TSMC to the West. If China wants to defeat the West, the quickest way would be to invade Taiwan and stop sending chips to the West. The West wouldn’t be able to produce defence equipment, continue its AI ventures and eventually go back to the Middle Ages.

So the catastrophe wouldn’t stop at not having the chips for iPhones, data centers and gaming, but it would be a ripple effect. True we have access to the old chips but I don’t see how we could win a war with TVs, washing machines and microwaves.

So I would bet the farm that the US would go full force to defend Taiwan. That is the main reason that while TSMC agreed to invest $100 billion in building semiconductors in the US, TSMC intentionally said that the most advanced chips would stay in Taiwan. This way they guarantee that the US would defend Taiwan at all cost.

I am no war strategist or expert but I think the US still has a military advantage over China. I found this video comparing the military assets of the US and China. The US beats China in the most relevant dimensions.

Also, I found this video analyzing 24 war simulations if China invades Taiwan. According to the video, the US wins in most scenarios and the critical piece is access to Japan’s airports. Yes, we should take this with a grain of salt because I don’t think the US would allow releasing a video that China would be successful but it is one more data point that the US still has the military advantage.

And no matter who is the real acting president of the US, be it Musk, Putin or Trump (in order of who I think most likely is the real acting president of the US), defending Taiwan is critical. Without TSMC, Musk can say bye-bye to his life mission of making humans a multi-planetary species, Putin could benefit in the short term but would become a junior partner in his alliance with China, and Trump’s macho and deal-maker look would evaporate, not to mention the stock market (the only external indicator Trump used to care about) would crash.

But let’s assume we are 100% certain that China will be successful at invading Taiwan.

Where should we invest?

Stating the obvious but the most direct impact would be on technology and consumer electronic stocks. Defence stocks may see short-term upside as the defence budgets of every relevant country would increase, but in the medium term, those stocks would collapse as well when they run out of advanced chips to produce those weapons. Shipping companies would be next as Taiwan is a key part of global shipping routes, which would also impact consumer staples, industrials and any sector that is left untouched. I could go sector by sector on how they would be destroyed if Taiwan is under Chinese control but then this thesis would be even longer.

So the only safe investment would be gold. Yes, if you think China will invade Taiwan, you should sell all your stocks, buy gold (and some guns) and stick your head under the sand.

That is my opinion. Let me offer you what the other side says so you decide.

My friend MJ thinks I am underestimating the probability of China invading Taiwan. Taiwan's political situation is fragile. China strongly desires to reunify Taiwan under its rule, and Xi Jinping personally sees this reunification as critical for his legacy.

If China invades Taiwan, the first target will be TSMC’s fabs as neither China nor the US would allow the other side to control them. Essentially, in a military conflict, TSMC’s fabs would likely be destroyed because they’re strategically critical to both sides. TSMC has 21 fabs out of which 16 are in Taiwan, two in the US, two in China and one in Japan (source).

The US currently has significant power to impose a high economic and political cost on China if it invades Taiwan. However, the US military advantage in the Pacific is declining. As time passes, the US might actually provoke China into acting sooner (while the US can still impose meaningful sanctions and military costs). Basically, the US might prefer China to attack sooner rather than later, thinking their leverage is stronger now than it might be in 5 or 10 years.

Xi Jinping’s political legacy depends heavily on reunifying Taiwan. If he fails to reunify Taiwan, it could undermine his entire leadership. Thus, China may become more aggressive if its economy weakens significantly. China might use nationalism (reunification) to restore public support if the economy struggles.

Risk #2. Reduction in AI-related spending

TSMC’s revenues grew 39% in the first two months of 2025, it was mainly driven by increased demand for AI chips. High-performance computing, which are the chips used for AI, represented 51% of total revenues in 2024 from 43% in 2023.

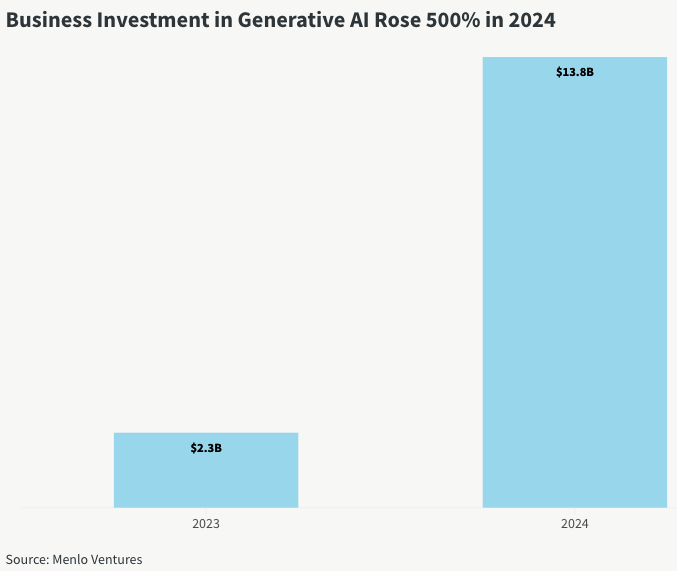

In 2024, investment in AGI (generative AI) rose 500% as companies were trying to capture the value from optimizing processes. IDC, expects investment in AI to grow from $228 billion to $632 billion by 2028, a 29% CAGR.

Deepseek only spent $6 million to develop its solution instead of the billions OpenAI, Microsoft, Meta and others have poured. However the market misunderstood the result, Deepseek’s result rather than decreasing the forecasted AI spending, will accelerate the growth. Businesses previously hesitant about investing millions in AI infrastructure might now embrace it due to significantly lower entry costs.

First of all, the lower cost would translate to higher adoption. Deepseek’s approach reduces the cost of deploying AI solutions, making AI accessible to a larger number of companies and applications.

Think about solar energy: When prices dropped, adoption skyrocketed—not decreased—because it became accessible for more households and businesses. Similarly, cheaper AI models mean more companies can afford to implement AI.

Also, lower-cost AI enables businesses to deploy it in more applications and smaller-scale solutions. AI won't just be for major tech giants; smaller businesses and startups can now afford to integrate AI into their products. This increased diversity of AI applications will drive up the demand.

As cheaper AI solutions enter the market, the total AI industry size expands rapidly. Even if individual deployments become cheaper, the sheer volume of deployments could more than compensate for the price reductions. More AI projects mean higher overall consumption of chips, storage, memory, networking components, and servers, all of which rely heavily on advanced semiconductors manufactured by TSMC.

Finally, Deepseek isn’t necessarily a direct competitor to ChatGPT; rather, it's complementary. It creates opportunities to implement AI where ChatGPT’s massive resource demands previously made it impractical or too expensive. Both can coexist, addressing different segments (enterprise vs. smaller businesses).

Risk #3: Competitive pressures from Intel and Samsung

I would be really surprised if Intel comes back and becomes a fearful contender. Keep in mind that in the past, under CEO Andy Grove, Intel was a formidable company. It was one of the 10X companies in Collins’ Great by Choice book (I strongly recommend the book). So maybe, somehow, Intel returns to its roots and returns to its motto ‘Intel Delivers’.

But it is a big bet.

So, the only real risk would be Samsung Foundry. Samsung Foundry is a division of Samsung Electronics. As of August 2024, Samsung Foundry was struggling to make a profit and said it needed more clients.

Samsung is actively working to enhance its competitiveness in the foundry sector by focusing on advanced process technologies and expanding its customer base.

If it succeeds, which I doubt based on TSMC’s strong moat explained earlier, it could take some market share from TSMC.

Risk #4: China’s Playbook: Undercut, Dominate, and Disrupt

China’s strategy has always been to outprice and eliminate rivals while moving up the tech and value chain. A clear example of China's strategy to underprice competitors and climb the technology value chain is the solar panel industry. Initially dominated by European and American companies, the market dramatically shifted around 2008–2012 when Chinese firms like Jinko Solar, Trina Solar, and JA Solar entered aggressively, using government subsidies, low-cost manufacturing, and large-scale production to flood global markets with cheaper products. Unable to compete, Western manufacturers like Germany's SolarWorld and America's Solyndra collapsed.

Once dominant, Chinese firms invested heavily in advanced technology, transitioning from lower-quality panels to high-efficiency products such as mono-crystalline and bifacial solar cells, and now control over 80% of the global solar supply chain.

One of my best calls of 2017 was Daqo New Energy (DQ), a polysilicon producer for solar cells located in China. Here is my thesis from that time and my closing.

Back to TSMC and the China risk…

China could aggressively push TSMC out of the legacy chip market by ramping up production at an unprecedented scale while refining its technological capabilities. China could flood the market with cheaper chips, erode TSMC’s dominance in older nodes, and weaken its financial strength. Backed by the Chinese government, these efforts will be shielded and subsidized for as long as necessary, with Beijing willing to absorb losses for years—an advantage TSMC simply doesn’t have. In that scenario, TSMC’s market share in legacy nodes could drop to 20%.

Risk #5: Trump’s tariffs

I don’t even think this is a plausible risk as Trump would make American companies less competitive as the raw material for its high-value product would be more expensive. But even if the tariffs are imposed, I am certain TSMC would pass that extra cost to its clients who would pass it to the final customers who wouldn’t even detect the price changes. (refer to the price increase exercise).

Conclusion

If you are reading this, kudos to you! 🎉

I won’t repeat or summarize what you just read—instead, I have something special for you.

If you made it through this 7,400-word deep dive, it means my approach to stock investing resonates with you, and I want to reward that.

As a thank you for your time and commitment, here’s an exclusive 75% discount on my paid subscription:

👉 Claim Your 75% Off Discount Here

This is my way of welcoming readers who truly engage with my work into the inner circle of serious investors.

Let’s keep compounding! 🚀

TSMC committed to build 4 fabs for $65 billion